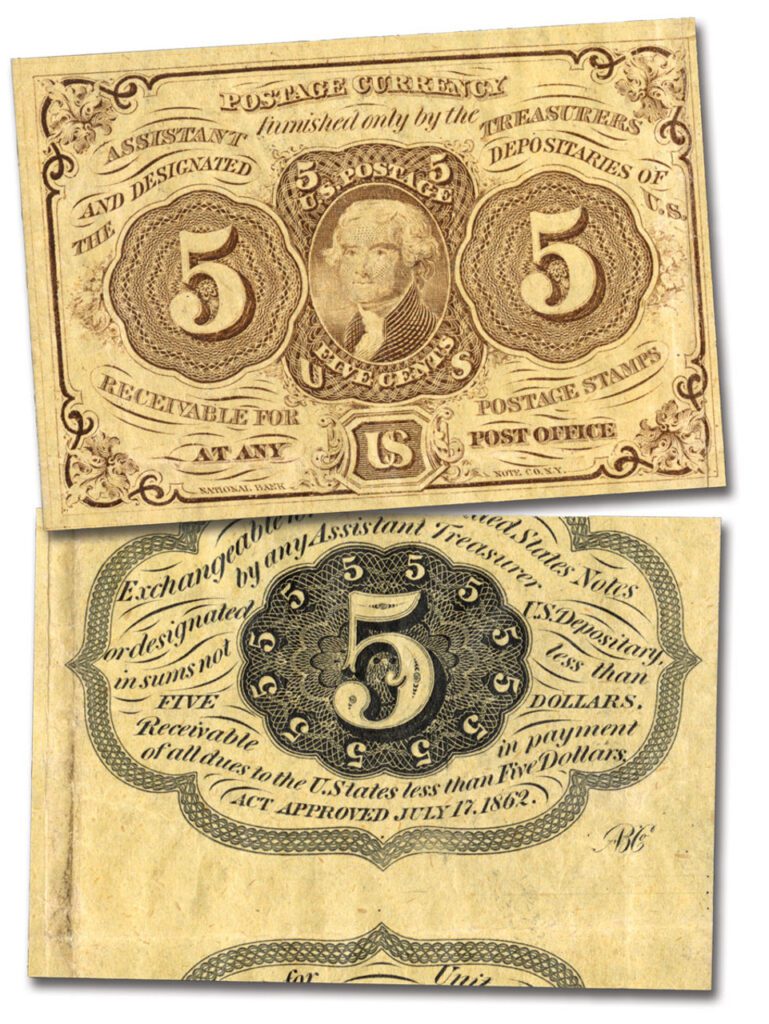

On March 10, 1862, the United States government issued its first widely circulated national paper money. These new notes, soon nicknamed “greenbacks,” were created during the financial strain of the American Civil War and transformed how the federal government financed itself.

Before 1862, most Americans used coins made of gold, silver, or copper for everyday transactions. Paper money existed, but it usually came from private banks rather than the federal government. Thousands of banks across the country printed their own notes. Each banknote had its own design and value. Some were trustworthy, but others were not. If a bank failed, its notes could become worthless. By the start of the Civil War in 1861, the country still lacked a uniform national paper currency.

The Union government soon faced enormous wartime expenses. It had to pay soldiers, buy weapons, build railroads, and supply armies spread across hundreds of miles. Early in the conflict, the government relied heavily on loans and new taxes. Those measures helped, but they could not cover the rapidly rising cost of the war.

Congress first experimented with a new form of federal paper money in 1861. These early bills were called Demand Notes. They were authorized in July 1861 and issued to help finance the first months of the war. Demand Notes were different from later greenbacks because they could be exchanged for gold coins at the US Treasury “on demand.” They also carried green ink on the back, which led people to begin calling them “greenbacks.” When wartime pressures forced the government to suspend gold payments later that year, the Demand Notes gradually disappeared from circulation.

Facing continued financial pressure, Congress passed the Legal Tender Act of 1862 on February 25, 1862. The law authorized the Treasury to issue $150 million in a new type of paper money known as United States Notes. These notes entered circulation on March 10, 1862.

Like the earlier Demand Notes, these bills had green ink printed on the back to discourage counterfeiting. The nickname “greenbacks” quickly became the common term for the new currency. Unlike the earlier notes, however, these bills could not be exchanged for gold or silver at the Treasury. Instead, Congress declared them legal tender, meaning they had to be accepted for most debts and payments within the United States.

Greenbacks were not backed by gold in the traditional sense. A gold-backed note can be redeemed for a fixed amount of gold at any time. Greenbacks did not offer that guarantee. Their value came from the authority of the federal government and from the requirement that they be accepted as payment.

However, gold still played an important role in the economy. Gold coins continued to circulate, and people often compared the value of greenbacks to gold. During the Civil War, greenbacks sometimes traded at a discount compared with gold. If confidence in the Union war effort dropped, it might take more greenbacks to equal the value of one gold dollar. When Union armies won important victories, confidence increased and the value of greenbacks usually improved.

Despite these fluctuations, greenbacks allowed the government to keep the war effort moving. They circulated widely in Northern states and quickly became a familiar part of everyday commerce. By the end of the Civil War, the government had issued about $450 million in United States Notes.

The introduction of federal paper money also helped reshape the nation’s banking system. Congress passed the National Banking Acts in 1863 and 1864. These laws created nationally chartered banks and a more uniform banking system. Banks that joined the system could issue national banknotes, but only if they purchased US government bonds as backing. This strengthened demand for federal debt and helped stabilize the nation’s currency.

In the years after the war, the United States gradually moved back toward a system tied more closely to gold. In 1879, the government resumed allowing certain paper notes to be exchanged for gold. Later, the Gold Standard Act of 1900 formally placed the US dollar on the gold standard, meaning the value of the currency was defined by a fixed quantity of gold.

American paper money continued to evolve during the twentieth century. New forms of currency appeared, including silver certificates and Federal Reserve Notes. The creation of the Federal Reserve System in 1913 established a central banking structure that still exists today. Federal Reserve Notes eventually replaced earlier types of paper currency as the main form of money in circulation.

United States Notes—the original greenbacks issued during the Civil War—remained part of the nation’s currency for more than a century. Although their role declined over time, they were printed in limited numbers until the late twentieth century.

| FREE printable This Day in History album pages Download a PDF of today’s article. Get a binder or other supplies to create your This Day in History album. |

Discover what else happened on This Day in History.